The Accounting systems

All departments in the program

Features

Features of all departments

Account Activity

In electronic accounting systems, account activity is all the financial transactions that affect a particular account. Account activity is used to create a record of all financial transactions that take place in a company, which helps to track money and prepare financial statements.

Account balances

- In electronic accounting systems, an account balance is the monetary amount in an account at a given time. The account balance represents the difference between the total debit and credit amounts in the account.

Trial Balance

- A trial balance is defined as a list that shows the balances of all accounts in a ledger. The trial balance is an important tool for businesses because it helps:Verifying the accuracy of accounting data: A trial balance is used to verify that the balances of all accounts are correct.Detecting errors: A trial balance can help detect errors in accounting data.Financial Reporting: A trial balance is used to prepare financial reports, such as the income statement and balance sheet.

cashbook

In electronic accounting systems, a cashbook is a place where a company's cash and other negotiable instruments are stored. Cashbooks are used to track all financial transactions that involve cash, which helps to prepare financial statements accurately.

Receipt and disbursement voucher

In electronic accounting systems, a receivable voucher is a document that proves the receipt of a monetary amount from a customer or third party. Receivable vouchers are used to track financial transactions that involve the receipt of funds, which helps to prepare financial statements correctly.

Accounting entries

An accounting entry is the process of recording financial transactions in a journal. Accounting entries are used to track all of a company's financial transactions, which helps to prepare financial statements correctly.

Cost centers

In accounting systems, a cost center is defined as a department or function within a company that is charged costs but does not generate direct revenues. Cost centers are used to track and analyze costs, which helps companies make better decisions about resource allocation.

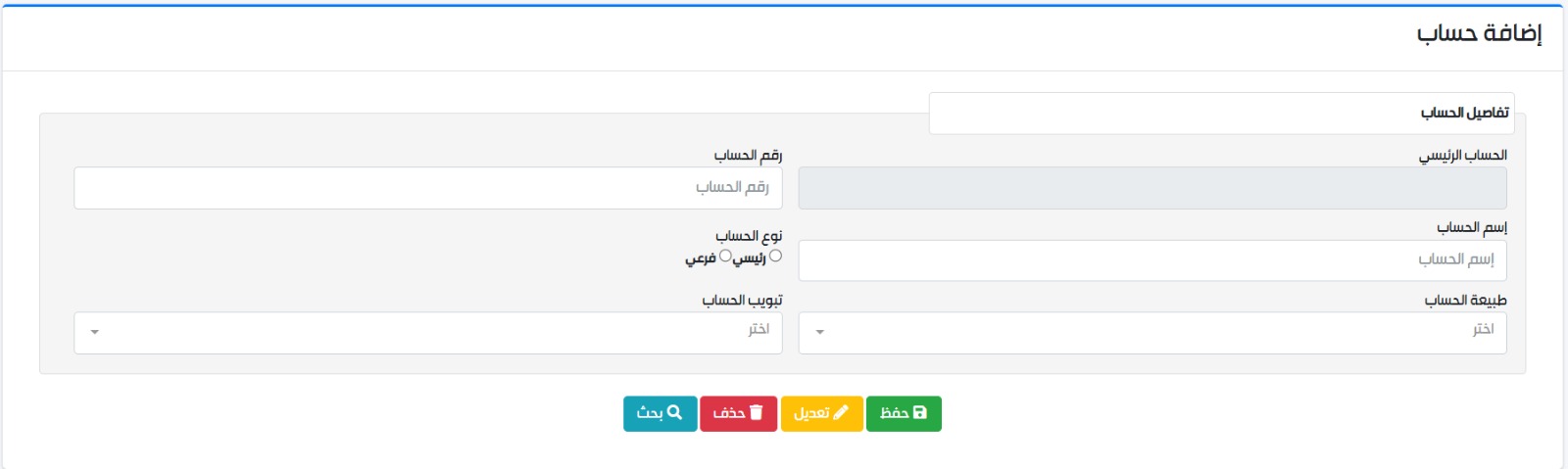

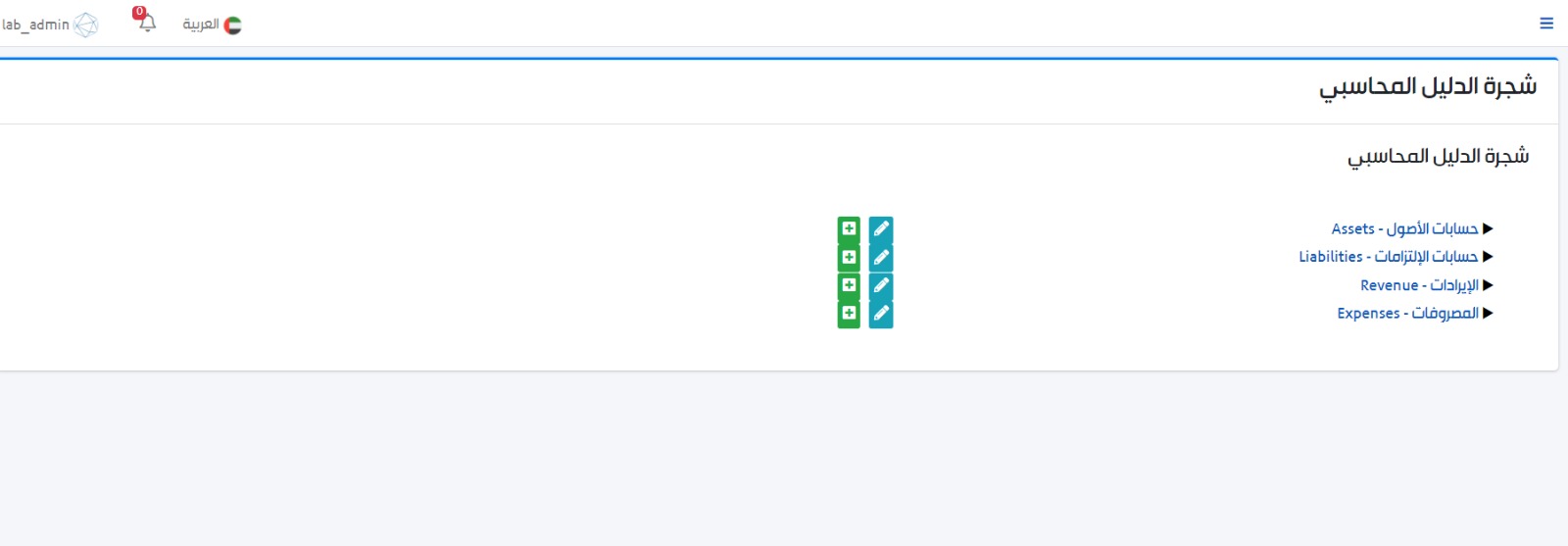

Accounting guide

In accounting, an accounting chart of accounts is a list of accounts that a company uses to track its financial transactions. The chart of accounts is used to organize financial data and make it more understandable.

fiscal year

In accounting systems, a fiscal year is defined as the period of time that is used to measure a company's performance. The fiscal year usually begins on a certain day of the year and ends on the same day of the following year.

revenues and expenses

In accounting systems, revenue is defined as the money a company earns from selling its products or services. Expenses are the money the company spends on operating its business.